I spent the morning at a breakfast with Carson Palmer, Ryan Tollner, and Katie Rodin. We talk a lot in real estate about “winning,” but these three have a different definition of it. Whether you are leading a brokerage, running a desk at a title company, or out there as an agent, their take on ethics hits home for our industry.

Character attracts character

Ryan Tollner is a top sports agent who admitted he entered a “slimy” business specifically to do it better at a higher level. He was very open about the fact that being ethical has cost him clients. In our world, we’ve all seen people say or do whatever it takes to get a listing or a signature. Ryan’s strategy is simple: position yourself as different. When you operate from a place of abundance, you realize there is enough business for everyone. You don’t have to chase the “scarcity” mindset that leads to cutting corners.

The “Double Life” trap

Katie Rodin made a point that every leader in our industry needs to hear: you cannot be one person in the office and another person out of the office. If you aren’t aligned, the cracks will eventually show. Carson Palmer backed this up, saying it is impossible to be consistent if you are cutting corners behind the scenes when no one is looking.

When the pressure is on and you’re tempted to take a shortcut, Carson’s advice is simple: pause and pray. He reminded us that your name is your only real currency. His athletes know they represent the name on the front of the jersey and the one on the back.

When things go sideways, don’t hide

We’ve all had a deal blow up or a mistake happen at the closing table. Katie’s advice for those moments is gold:

Make it right immediately.

Reverse engineer the mistake to make sure it doesn’t happen again.

Lead by example. Don’t hide behind your title when you mess up.

Creating a safe space for your staff and agents to own their mistakes is how you actually eliminate them in the long run.

Coaching the person, not the production

Carson mentioned that when an athlete’s performance drops, he looks at what’s going on in their life. Whether it’s a kid or an NFL pro, the human needs are the same. If an agent or a staff member is struggling, ask about the underlying issue. Usually, if you coach the person, the performance turns around on its own.

The support system

One thing that really stuck with me was Katie mentioning her spouse is a critical part of her success. In real estate, our families feel the heat of our schedules as much as we do. Acknowledging that support system is part of being an authentic leader.

In an industry where our reputation is everything, these reminders are a great gut check. A reminder that playing the long game is how we win the day.

As I was listening to the Fed statement this week, my ears perked up. As many of you know, my daily reality is a bit of a balancing act. Besides being the Managing Partner of a real estate staffing firm and a licensed CA real estate broker, I teach these concepts at the Masters, Bachelors, and Associate / Certificate levels. Whether I am in the boardroom or the classroom, I am looking for the signal through the noise.

The Fed just released its decision to keep interest rates steady at a target range of 3.5% to 3.75%. While “no change” might sound like stability, the real story is in how the Fed is grappling with a sudden shift in the economic landscape.

The moment the conversation turned to the Phillips Curve, I knew we were at a turning point and a teaching example for my students. While this sounds like academic jargon, for those of us in real estate, it is the “Floor of Truth” the Fed uses to decide the cost of your next project.

The Fed’s Dual Mandate: The Goalposts

To understand today’s “hold,” you have to remember the Fed’s two assigned goals for monetary policy:

Maximum Employment: Promoting a labor market where anyone who wants a job can find one.

Price Stability: Keeping inflation in check, with a long-standing target of 2%.

Today’s decision is a direct result of the Fed trying to balance these two competing goals amidst global volatility.

What is the Phillips Curve?

In 1958, an economist named A. William Phillips noticed a pattern: an inverse relationship between unemployment and wage growth. Later, economists made the connection to inflation explicit.

The Logic: When unemployment is low, the labor market is “tight.”

The Chain Reaction: Employers offer higher wages to attract talent; those workers spend more, which drives up prices.

The Historical Trade-off: For decades, it was believed you couldn’t have both low unemployment and low inflation simultaneously. If you wanted to kill inflation, you had to accept higher unemployment.

Why the Rules are Breaking in 2026

In the years leading up to 2020, the curve “flattened” meaning we had record-low unemployment without a massive spike in prices. But today, the situation has reversed and become much more complex.

The Current “Ambiguity Gap”:

We are currently seeing low unemployment, but inflation is not cooling off. Instead, core inflation is sitting at roughly 3.3%. This is being pushed higher by soaring oil prices linked to the Middle East conflict and new tariffs. This defies the “soft landing” narrative and creates a massive gap in the data where old-school models are failing to explain the present.

Strategic Deep Dive: Has Globalization Dismantled the Model?

One of my Masters level students, Enyo, raised a sharp point in our discussion: Does the globalization of the economy essentially dismantle the direct relationship between inflation and unemployment?

Powell admitted yesterday that our current inflation isn’t reacting to “standard Phillips Curve” policy. Instead, he is citing the “runoff” of one-time shocks like tariffs that take a year to bleed through the system.

Globalization has changed the game. While inflation is now globalized through trade and energy, real estate remains fundamentally local. You cannot outsource a framing crew or a property manager. This creates a disconnect: we face global capital costs, but we still rely on local wage elasticity to drive our rents.

The Executive Lesson: Synthesis over Certainty

Chairman Powell’s focus on these models tells us the Fed is in a high-stakes moment of Synthesis. They are trying to determine if the relationship between jobs and prices has fundamentally shifted due to these outside shocks.

In our industry, we face this daily. You might see low vacancy rates but stagnant rent growth due to outside economic pressures. When the standard models don’t make sense, your value as a leader isn’t just in your IQ: it’s in your Judgment to see the truth amidst the noise.

The Takeaway: The Fed is holding steady because the “rules” of the Phillips Curve are being rewritten by global conflict and trade policy. They are choosing Functional Decisiveness, holding the line rather than making a “perfect” move that might arrive too late to save the economy from these new inflationary shocks.

“All great undertakings do not consist of doing again what others have done before, but in recapturing the spirit that went into what they did.”~ Paul Valéry, The Collected Works

Every market produces its legends.

The agent who dominated a farm area for twenty years. The MLO who built a referral network so deep they never ran a cold lead. The recruiter who had a sixth sense for talent and almost never got it wrong.

And every generation tries to copy them.

They study the scripts. They reconstruct the systems. They read the books, attend the events, and try to reverse engineer the moves that made those people great.

It rarely works. Not because the information is wrong. Because the information is not the point.

What made those producers exceptional was not the specific action they took. It was the thinking behind it. The belief that relationships compounded over time. The conviction that the market rewards consistency when everyone else is chasing momentum. The discipline to do the unsexy work when the results were not yet visible.

That is what Valéry is pointing at. Not the tactic. The spirit.

If you want to build something that lasts in this business, do not ask what the greats did. Ask why they did it. Ask what they believed about people, about service, about the long game, that made those actions the obvious choice.

Then ask yourself what those same beliefs look like in your market, with your clients, in this moment.

The script they used in 2004 will not close the client in front of you today. But the mindset that built that script absolutely will.

Do not imitate the act. Carry the spirit forward.

Over the last few posts we did exactly that. Simplify. Survive. Stay grounded. Embrace the hard. Build something that lasts.

“This is how we grow: by being defeated by greater and greater things.” ~ Rainer Maria Rilke, The Book of Images.

There is a moment in every real estate or mortgage career when the challenge in front of you is bigger than anything you have handled before.

Maybe it is your first luxury listing in a neighborhood where the clients expect a level of service you have not delivered yet. Maybe it is a complex commercial deal with moving parts you are still learning. Maybe it is building a team for the first time and realizing that leading people is an entirely different skill than producing.

Most people in that moment feel like they are failing. They are not. They are growing.

The problem is we have been conditioned to treat difficulty as a signal to stop. To pull back. To find the lane that feels more comfortable. But discomfort is not a warning. It is a marker. It tells you exactly where your edge is.

The agent who only takes the listings they are certain to win never finds out what they are actually capable of. The MLO who only works the loan types they know cold never builds the range that separates good from exceptional.

Rilke was not writing about real estate in 1902. But he understood something about ambition that applies to every producer in this business. The things that stretch you, shake you, and occasionally beat you are not obstacles to your growth. They are the mechanism of it.

You do not grow by mastering what is already easy. You grow by taking on what is just beyond you and staying in the fight long enough to figure it out.

The next time a deal, a client, or a challenge makes you feel overmatched, pay attention to that feeling. It means you are in the right room.

But after reading the study again, I’ve had a second realization that hits even harder. It isn’t just about what the tech can do. It’s about what it can’t touch.

The Knowledge Worker’s Reckoning

For decades, we told everyone that the “safe path” was white collar. We said stay out of the sun, keep your hands clean, and get a degree that puts you behind a desk. We thought the “process” of our jobs was our protection.

We were wrong. The plumbers business just became more valuable! The report makes it clear that the more educated and process heavy a job is, the more at risk it is. What happened to blue collar workers thirty years ago is happening to office workers right now.

But look at what the report says is actually safe:

Construction and Trades

Food service

Grounds maintenance

Personal care

This past month, my house was a revolving door for tradespeople: two plumber visits, an HVAC tech, and an exterminator. Between a dead hot water pump, a leaky faucet, cooling issues, and an ant invasion, I’m out $1,200.

As I watched them work, it hit me: You can’t “prompt” a HVAC unit into fixing itself.Ants don’t care about large language models. These problems require physical intervention, not digital processing. In an era where AI is coming for every desk job, it’s clear: Blue is the new white.

What This Means for Us

For broker owners, recruiters, and high performers in mortgage and title, this is the new strategy. We have to stop acting like information gatekeepers and start acting like complex problem solvers.

The “blue” in our world isn’t about tools; it’s about the grit of the human experience:

For Brokers and Recruiters: Stop recruiting for “process.” Any agent can put a house on the MLS. Recruit for empathy and the ability to negotiate. Don’t ask a recruit about their tech stack. Ask them how they handled a deal that was falling apart at 5:00 on a Friday. That is the only skill that isn’t being automated.

For Top Agents: The transactional agent is a dinosaur. The advisor is the future. AI can find the comps, but it can’t tell a seller why they shouldn’t take the highest offer because the terms are shaky.

For Loan Officers and Title Reps: Production is exposed. Your value is now accountability. A bot can draft a document, but it can’t stand in front of a client and take responsibility for it. It can’t walk a family through the “messy middle” of a complicated file.

Moving Up

The takeaway from Phase 2 is simple: Don’t fight the 90 percent. If AI can handle the checklists and the data entry, let it.

That isn’t a threat to your business. It’s a gift of time. Use that time to double down on the things machines can’t touch: social sensitivity, storytelling, and high level judgment.

The era of being paid just to move information is over. The human era, where we are paid for our presence and our ability to navigate the physical and emotional world, is just beginning.

Blue is the new white. If you want to Win the Day, stop being a processor and start being the person who knows how to fix the pump.

Let’s get to work.

PS: Want a list of killer interview questions to find the agents who actually have this grit? Ping me.

A System Will Produce What A System Will Produce, Nothing Less and Nothing More!

You will see it this week. Maybe you already have.

The agent who cut corners and still closed the deal. The MLO who overpromised and somehow kept their clients. The recruiter who hired fast, skipped the culture fit, and got away with it.

And somewhere in the back of your mind a quiet, dangerous thought shows up. Maybe that is just how it works.

It is not.

Here is what is actually happening. The negative examples are loud. They spread fast. They get shared, screenshotted, and turned into cautionary tales that somehow also feel like permission. Bad behavior stirs emotion. And emotion travels.

Good behavior does not work that way. The agent who spent three years building a referral network through genuine relationships does not make the highlight reel. The MLO who called every client back within the hour, every time, for a decade does not go viral. The transaction coordinator who caught the error that saved the deal does not get a LinkedIn post.

But those people exist. In every market. In every office. In every brokerage you have ever walked through.

The question is not whether the bad examples are real. They are. The question is whether you are going to let them set the standard.

Your clients are watching how you operate. Your team is watching. The newer agents in your office are watching more than you think.

You are someone’s role model whether you signed up for it or not.

Good news is always quieter than bad news. That does not make it less true. Keep doing the work the right way. The market has a long memory, and so do the people who matter most in your business.

A few of my readers have asked me to re-cap what happened in the U.S. Senate today – here is my take:

On March 12, 2026, the Senate overwhelmingly passed the 21st Century ROAD to Housing Act in an 89–10 vote. This landmark bipartisan legislation led by Senate Banking Committee Chairman Tim Scott (R-SC) and Ranking Member Elizabeth Warren (D-MA) represents the most significant federal housing overhaul in decades.

The bill combines the Senate’s “ROAD to Housing Act” with the House’s “Housing for the 21st Century Act” to address the national shortage of nearly 4.7 million homes.

Executive Summary

The primary goal of the Act is to boost housing supply and lower costs by cutting federal “red tape,” modernizing aging housing programs, and incentivizing local governments to reform restrictive zoning and permitting rules. While largely praised for its supply-side reforms, the bill includes a controversial provision targeting corporate landlords that has sparked intense debate among industry stakeholders.

Key Highlights & Provisions

1. Restrictions on Institutional Investors (Section 901)

The most discussed addition is a provision titled “Homes are for People, Not Corporations.”

The Ban: Prohibits “large institutional investors” (entities owning 350 or more single-family homes) from purchasing additional single-family properties.

Build-to-Rent (BTR) Mandate: Requires institutional investors to sell build-to-rent homes to individual buyers within seven years of construction.

Controversy: Critics, including the National Association of Home Builders and the U.S. Chamber of Commerce, argue this will stifle investment and could slash single-family production by 40,000 units per year.

2. Cutting Regulatory Red Tape

Environmental Streamlining: Categorically excludes certain low-impact projects (like infill and rehabilitation) from rigorous NEPA reviews to speed up construction.

Pattern Book Grants: Provides funding for cities to adopt “pre-approved” building designs, allowing developers to bypass lengthy permit approvals for standardized housing types.

Rural Housing Reform: Streamlines the joint review process between HUD and the USDA for projects receiving funding from both agencies.

3. Modernizing Federal Grants (HOME & CDBG)

CDBG Flexibility: For the first time, allows Community Development Block Grant (CDBG) funds to be used for new housing construction (previously limited to rehabilitation).

Incentive Adjustments: Starting three years after enactment, CDBG funding may be adjusted by 10% based on a community’s actual housing production.

HOME Program: Expands income eligibility to better support “workforce housing” and authorizes funds for infrastructure (like water/sewer) adjacent to housing projects.

4. Supporting Diverse Housing Options

Manufactured Housing: Updates federal rules and provides grants (via the PRICE program) to preserve and maintain manufactured home communities.

RESIDE Act: Authorized to help local governments convert vacant or abandoned commercial structures into “attainable housing.”

Public Welfare Cap: Increases the cap on bank “public welfare investments” from 15% to 20%, encouraging more private bank capital to flow into affordable housing.

5. Unexpected Provisions

CBDC Moratorium: Includes a temporary ban on the Federal Reserve issuing a Central Bank Digital Currency (CBDC) through 2030, a priority for some conservative lawmakers.

What’s Next?

The bill now returns to the House of Representatives. While the House passed a previous version 390–9, leaders like Financial Services Chair French Hill (R-AR) have signaled that the Senate’s new investor restrictions and the removal of certain community banking provisions may require further negotiations or a conference committee to reconcile the two versions.

We talk a lot about confidence in this business. We talk about the mindset it takes to knock on a door after a rejection, to pick up the phone after a dead lead, to walk into a listing appointment after losing the last three.

What we do not talk about enough is where that confidence actually comes from.

It does not come from winning. Not entirely.

Winning builds your skill. It teaches you what works, sharpens your process, and gives you the evidence that you are capable. Every closed deal, every funded loan, every signed contract is a data point that says you know what you are doing.

But winning does not teach you what to do when it falls apart.

That is what failure does.

Every deal that blew up at the title table. Every client who went with another agent after three months of your time. Every rate lock that expired at the worst possible moment. Those are not just painful memories. They are proof that you survived. That you came back. That the ground did not swallow you whole.

When the next hard thing comes, and it will, your brain does not just ask “can I do this?” It also asks “have I been here before?”

If the answer is yes, the fear shrinks.

This is why veterans in this business carry themselves differently. Not because everything went right for them. Because enough went wrong and they are still here.

Do not waste your failures. They are building something in you that success never could.

Your pipeline is full. Your calendar is stacked. You have three offers pending, two listings coming, and a referral partner who wants lunch this week.

And somehow, nothing is moving.

Here is what most high performers do in that moment. They add. Another system. Another tool. Another meeting. Another strategy session with themselves at midnight.

Wrong direction.

When performance stalls, the instinct is to do more. But more is usually not the problem. More is usually the symptom.

The best agents and MLOs I have watched work through a plateau did not find their way out by adding. They found it by cutting. They dropped the two clients who were consuming 40% of their energy and producing 10% of their revenue. They stopped attending the networking event that felt productive but never converted. They deleted the apps that created the illusion of work without the output.

Clarity is not something you find. It is something you uncover.

Think about your business right now. Not the version you are building toward. The one you are actually running today. What is on your plate that does not belong there? What are you holding onto because you said yes six months ago and do not know how to say not yet?

A transaction coordinator who is stretched across too many files makes mistakes. An MLO chasing every lead type closes none of them well. An agent who is everything to everyone becomes nothing to the right client.

Subtraction is not giving up. It is getting precise.

The most dangerous word in a high performer’s vocabulary is not no. It is yes, said to the wrong thing at the wrong time.

So before you build a new plan, audit the current one. Not for what to add. For what to remove.

When you need clarity, subtract.

Over the next few posts we will do this together. Simplify. Survive. Stay grounded. Embrace the hard. Build something that lasts.

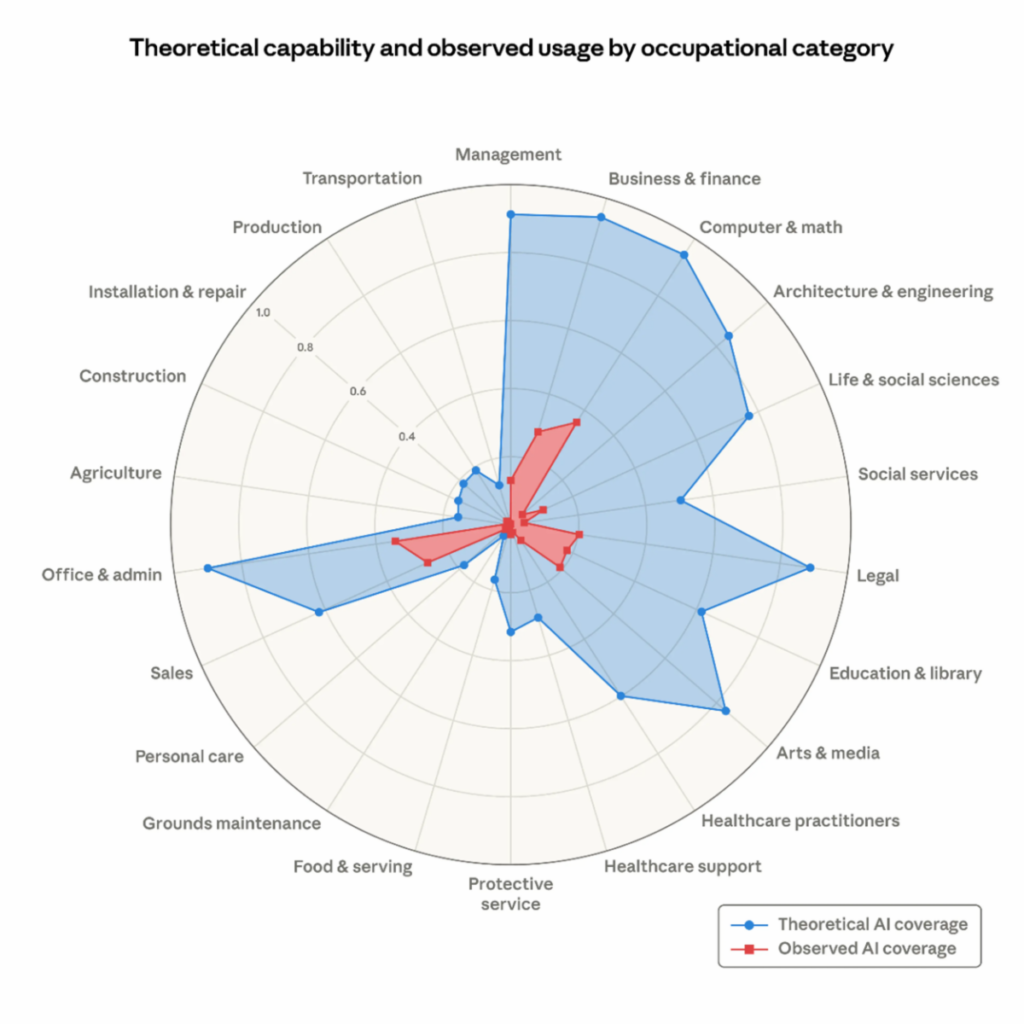

A brand new study dropped this week that every real estate professional needs to read. Not to panic. To plan.

The research, published March 5th by Anthropic economists Maxim Massenkoff and Peter McCrory, is titled “Labor market impacts of AI: A new measure and early evidence.” Here’s the number that stopped me cold: AI is theoretically capable of handling 94% of tasks in computer and math occupations, and 90% in office and administrative roles, yet it’s only being used for about 33% of them in actual professional settings right now.

That gap is not permanent. It is closing. And our industry is in its path.

The workers most exposed are not warehouse employees or entry-level staff. They are the educated, higher-earning, white-collar professionals. The lawyer. The financial analyst. The mortgage originator. The transaction coordinator. The people whose jobs are built around documents, information, and process. That’s our world.

Here’s the part I want you to hold onto: the study also found no significant increase in unemployment for high-exposure workers yet. This is not a cliff. It is a slow shift. And that means the professionals who act now will be the ones who are left standing when it levels off, doing very well, because there will be fewer of them serving the same volume of business.

Geoff Colvin wrote about this in his book “Humans Are Underrated” back in 2015. His thesis was simple: stop trying to compete with machines at what machines do. You will lose that contest. Instead, he argued, build the four things humans do that technology has never been able to replicate: empathy, social sensitivity, storytelling, and relationship building.

Read that list and think about the best agent, the best MLO, the best title rep you know. That is exactly what they do every single day. The question is whether you’re building those skills intentionally or just hoping they carry you.

Your Role. Your Risk. Your Move.

If you’re a Transaction Coordinator, here’s the honest truth: the checklist version of your job is going away. Document collection, deadline tracking, compliance checklists, status updates, AI is being purpose-built to automate exactly those tasks. The TCs who thrive will be the ones who lead with Colvin’s skills. Client communication when things go sideways. Emotional steadiness when a deal is falling apart. Problem escalation that requires a human judgment call. Start making that shift now, before someone makes it for you.

If you’re a Mortgage Loan Originator, rate shopping, guideline matching, and doc review are in the crosshairs. What AI cannot do is sit across from a self-employed borrower with three LLCs and a complicated return and build enough trust to get the deal done. It cannot call a first-time buyer at 9pm before a rate lock expires and talk them off a ledge. The MLOs who survive will own the complex, the non-QM, the jumbo, the scenarios where empathy and expertise are the actual product.

If you’re in Title and Settlement, the production side is highly exposed. Title search, commitment prep, back-office review, that is document analysis and legal pattern matching. AI is very good at exactly that. Title sales is a completely different story. The referral relationships you’ve built with agents and lenders through years of showing up, solving problems, and following through are not automatable. That is relationship building and social sensitivity in action. Protect and grow that side of your business aggressively.

If you’re a Real Estate Agent, you are actually more resilient than most headlines suggest. Physical presence, emotional attunement, local expertise, negotiating across a table, those are genuinely hard to replicate. Your real risk is the transactional end: the buyer’s agent whose primary value is delivering information that buyers can now find for free on their phone. The agents who survive will be the ones who lead with Colvin’s four skills every single day. The ones who tell the story of why this home fits this family’s life. The ones who read the room in a negotiation. The ones whose clients call them back for every transaction because the relationship is real.

The Practical Moves That Matter

Get fluent in AI tools before someone forces you to. The professionals who already know how to use them will be training others, not replaced by them.

Specialize in the complex. Luxury clients, distressed properties, non-QM borrowers, estate sales, 1031 exchanges. The messy, human-intensive scenarios are your moat. Generalists are more replaceable than specialists. Always have been.

Own the judgment and accountability layer. AI can draft a contract. It cannot be held liable for the advice behind it. The agent, the originator, the title officer who stands behind the recommendation and shows up when things go sideways, that person still has a job. Always will.

Use AI to handle the process so you can focus on people. The professionals who thrive won’t fight these tools. They’ll use them to do in two hours what used to take two days, and put that time back into relationships, prospecting, and the conversations that actually move the needle.

Colvin had it right a decade ago. AI is taking the process. Your job is to be human. Lead with empathy. Read the room. Tell the story. Build the relationship.

Sources: “Labor market impacts of AI: A new measure and early evidence” by Maxim Massenkoff and Peter McCrory, Anthropic, March 5, 2026. “Humans Are Underrated: What High Achievers Know That Brilliant Machines Never Will” by Geoff Colvin, Portfolio/Penguin, 2015.